In the eleven days between 15 May and 26 May 2026, fuel in Delhi got expensive in a way that did not produce any headlines. Petrol crossed ₹102 a litre, diesel went over ₹95, CNG climbed past ₹83 a kilogram, and nobody held a press conference about it. Oil marketing companies revised retail prices four times. Indraprastha Gas Limited revised CNG four times. Each individual hike was small — a rupee here, two rupees there. The cumulative effect was the steepest sustained rise in pump prices since May 2022. By 26 May, a middle-class household running one car and one two-wheeler in the National Capital Region was paying close to ₹2,000 more a month than it had at the start of the financial year, on the same set of trips, the same school runs, the same office commutes.

This is not a crisis in the way most crises are framed in Indian journalism. It produces no riots. It generates no electoral slogans. It does not, on its own, push families into formal poverty. What it does, quietly and steadily, is shrink the gap between income and outgo for the urban Indian middle class — a class that is asked, year after year, to absorb every shock between the global economy and the political economy of energy taxation, while being told that things are fine. Fuel is the most reliable mechanism by which the world’s volatility enters an Indian household. The 2026 hikes are a reminder, written in rupees on a pump display, of how that mechanism works.

What is actually happening at the pump

The bare facts first. On 26 May 2026, the Indian Oil Corporation website listed petrol in Delhi at ₹102.12 a litre, diesel at ₹95.20. In Mumbai, petrol was ₹111.21 and diesel ₹97.83. In Chennai, Kolkata and Bengaluru, the rates differed slightly because of state VAT structures but all sat at near-2022 highs. Indraprastha Gas Limited, which retails CNG in Delhi, Noida, Greater Noida, Ghaziabad, Faridabad, Gurugram and several adjoining cities, raised CNG in the capital by ₹2 a kilogram on 26 May to ₹83.09. Noida and Ghaziabad reached ₹89.7 before the latest revision. Gurugram sat at ₹86.12. The Tribune, BusinessToday and Zee Business all carried the IGL release. None of these revisions made it to the front page of any major daily.

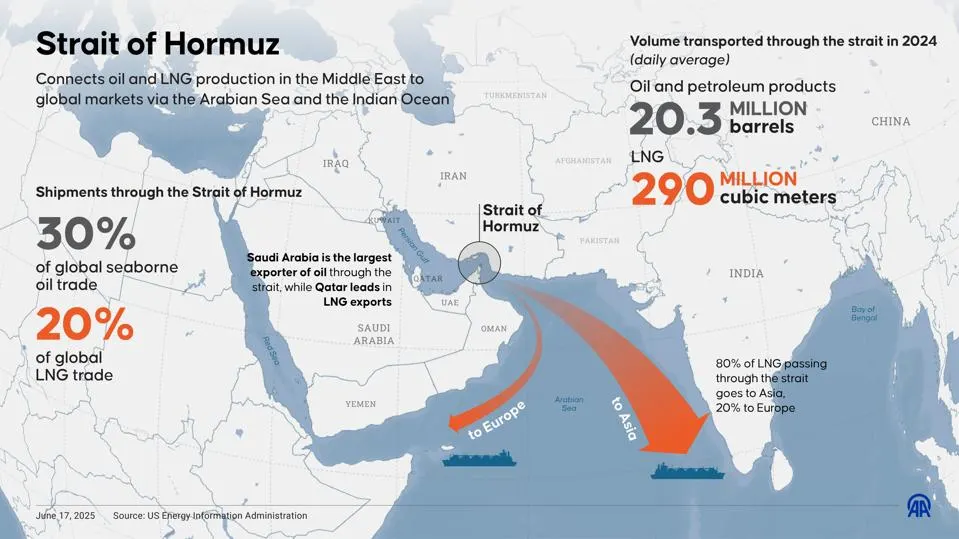

The trigger for the rise is unambiguous. The 2026 Strait of Hormuz crisis, which began with US and Israeli strikes on Iran on 28 February, has compressed global oil and gas supply chains, raised tanker insurance and freight rates, and pushed Brent crude from comfortably below $75 a barrel at the start of the year to over $110 in late May, before easing on hopes of a US-Iran ceasefire. Roughly 45 to 50 per cent of India’s crude imports and over half of its natural gas imports normally transit through the strait, according to credit rating agency ICRA. When the corridor became a war zone, every barrel and every cargo of LNG that India bought became more expensive, even when it arrived through a different route.

The Centre saw the wave coming. On 27 March, the Ministry of Finance issued a Gazette notification cutting the Special Additional Excise Duty on petrol from ₹13 a litre to ₹3 and effectively eliminating it on diesel, while introducing export duties of ₹21.5 a litre on diesel and ₹29.5 on aviation turbine fuel to keep domestic supply prioritised. The duty cut absorbed part of the global rise. It did not, in the end, fully neutralise it, because crude kept climbing through April and most of May, the rupee weakened, and oil marketing companies — which had absorbed losses through much of 2024 and 2025 to keep prices steady — eventually passed the residual cost on to consumers.

Where every rupee at the pump goes

Few household expenses are as opaque as fuel. To understand why prices feel sticky, it helps to look at what each litre actually contains.

At the base sits the cost of refined product, derived from the price of crude oil and the rupee-dollar exchange rate, plus refining margin and ocean freight. After 27 March 2026, central excise duty on petrol is around ₹3 a litre (down from ₹13) and on diesel close to zero (down from ₹10). State VAT comes on top — 19.4 per cent of the chargeable price in Delhi for petrol, with diesel taxed at lower rates; Maharashtra applies a 26 per cent VAT plus ₹5.12 a litre additional levy in Mumbai, Thane and Aurangabad, and 25 per cent plus ₹5.12 in the rest of the state. Dealer commissions, typically in the range of ₹3.50 to ₹4 a litre, sit at the end of the chain.

The reason petrol prices vary across states, in other words, is not refining or freight, both of which are broadly similar across India. It is state VAT. This explains why petrol in Mumbai is nearly ten rupees more expensive than in Delhi at the same crude-price moment, and why Andhra Pradesh — which charges 31 per cent VAT plus ₹4 a litre plus a road development cess — consistently has the highest retail petrol in the country. The same logic plays out for diesel, with smaller variation because diesel VAT is generally lower than petrol VAT across most states.

For CNG, the build-up is different. Compressed natural gas is sold by city gas distribution companies — IGL in Delhi-NCR, Mahanagar Gas in Mumbai, Adani-Total Gas across western India, and so on — at prices that incorporate domestic gas price under the Administered Price Mechanism, the cost of imported LNG to fill any shortfall, network operating costs, and state VAT. The IGL hikes through May 2026 reflect the rising cost of imported LNG after Qatar’s force majeure declaration on the Petronet contract, plus rupee weakness against the dollar. The four hikes were 50 paise, 80 paise, ₹1 and ₹2 in quick succession. Each was small in isolation; together they added more than ₹4.50 a kilogram to the Delhi CNG rate within a fortnight.

Why petrol and diesel are still outside GST

A reader’s reasonable question, looking at this layered tax structure, is why the Goods and Services Tax, introduced in 2017 precisely to standardise indirect taxation, has not been extended to petrol and diesel. The legal mechanism exists. When GST was introduced, petroleum products were placed outside the regime with the explicit option of bringing them in later through a GST Council decision. The political mechanism has not delivered.

The reason is straightforward. Fuel taxes are one of the most reliable revenue streams for both the Centre and state governments. Demand is inelastic — people who need to commute will fill up regardless of price within a wide range. Collection is centralised at depots, evasion is difficult, and the volumes are predictable. Central excise on petrol and diesel together yielded ₹3.71 lakh crore in 2020-21, according to Petroleum Ministry data, and remained a major contributor to central tax receipts in subsequent years. State VAT on fuels funds a significant share of state budgets, particularly for states without strong industrial bases.

Bringing petrol and diesel under GST would standardise rates — most likely capping them at 28 per cent plus a cess — but it would also force the Centre and the states to share the revenue under the GST distribution formula. No state finance minister has, in living memory, voluntarily surrendered a captive revenue stream. Finance Minister Nirmala Sitharaman has repeated, including at the GST Council meeting of June 2024, that the Centre is willing but the decision rests with the states. The states have not moved. As long as that political equilibrium holds, fuel will remain the most heavily taxed essential commodity in the Indian basket, and households will absorb the resulting volatility.

The middle class as shock absorber

It is worth saying plainly that the Indian middle class has, for the better part of fifteen years, been the country’s most reliable shock absorber. EMIs have risen with the RBI’s tightening cycle. Rents have climbed across metro and tier-one cities, particularly after the return-to-office trend of 2023-24. School fees and healthcare costs have outpaced headline inflation by a wide margin. Salary growth in many service sectors has slowed. Into this already squeezed budget, fuel has now added a recurring, unavoidable expense.

The most exposed within this class are those whose income does not adjust to inflation in real time. Autorickshaw drivers in Delhi run a CNG cost that has risen by nearly ₹5 a kilogram in twelve days, on fare structures regulated by the state transport department that have not been revised. App-based cab drivers face the same squeeze, with aggregators slow to update per-kilometre rates. Delivery riders on bike fleets absorb fuel hikes against fixed per-order payouts. School bus operators have begun quietly raising charges for the new academic session. Small traders running diesel-fired generators for shop lighting in towns with unreliable power face higher operating costs they cannot fully pass on. These are people the Reserve Bank’s policy statements do not name but whose budget compression is the social cost of every Hormuz crisis.

The EV question

A natural reader response to all this is: should I switch to an electric vehicle? The honest answer is more complicated than the marketing brochures suggest.

Electric two-wheelers and three-wheelers have made meaningful progress in Indian cities, supported by lower running costs (₹0.40 to ₹0.80 a kilometre for an electric scooter versus ₹2.50 to ₹3 for a petrol equivalent), the FAME-II subsidy regime, state-level incentives in Delhi, Maharashtra, Gujarat and Tamil Nadu, and improving battery technology. Electric autorickshaws have seen real fleet conversion in cities like Delhi and Hyderabad. For these segments, the case is fairly clear.

Electric cars are a different proposition. The upfront price premium relative to a petrol-equivalent variant remains substantial, charging infrastructure is uneven outside the top eight metros, battery replacement costs ten years down the line are still a question mark, and resale values are not yet established. For a household running 50 to 80 kilometres a day in an EV-friendly city, the maths can work. For households running fewer kilometres or living outside the major metros, the payback period stretches into the high single digits, by which point fuel prices may have moved in either direction.

The deeper question, which most EV coverage skips, is where the electricity itself comes from. India’s grid still depends on coal for roughly half of generation, with renewables expanding fast but not yet dominant during the evening peak when most household charging happens. Switching to an EV shifts the inflation exposure from imported crude to domestic coal and grid tariffs, both of which carry their own risks. EVs will, over the next decade, reduce India’s fuel import bill in aggregate. They will not insulate any single household from energy price swings.

What rural India is paying

The urban middle class gets most of the column inches in fuel coverage. Rural India absorbs a parallel shock that is rarely framed in fuel terms. Diesel pump-sets running irrigation in states like Punjab, Haryana and parts of Uttar Pradesh face higher operating costs every season. Tractors used in land preparation for both kharif and rabi cycles consume diesel that has risen even with the excise cut. Trucks moving farm produce from mandis to urban markets — and the same trucks bringing fertiliser, seeds and pesticides back — all run on diesel. The rural cost of a fuel hike does not show up in a Delhi headline; it shows up in the gross margin of a small farmer in Vidarbha or in the per-quintal price difference that a Kanpur trader charges for atta.

What most reports are missing

Most fuel-hike coverage frames the story as a transport or commuter problem. Two angles get under-reported.

First, the role of the rupee. A weaker rupee can do almost as much damage as a higher crude price. When the rupee touched ₹95.22 to the dollar in March and stayed weak through April and May, every barrel of crude India imported became more expensive in rupee terms, even when Brent eased. The exchange rate is the silent multiplier on every Hormuz development, and most consumer-facing coverage ignores it.

Second, the deferred bill. Oil marketing companies absorbed sizeable losses through 2024 and 2025 to keep retail prices stable, and the 27 March excise cut absorbed more. Those absorbed costs do not vanish. They show up either as lower oil-company profits — which flow through to lower central tax receipts on those profits — or as deferred price hikes when fiscal space tightens. The middle-class bill is, in effect, being paid in instalments across multiple years.

What happens next

Three trajectories are worth tracking. If the US-Iran ceasefire firms up through June and the strait reopens, Brent could ease back toward $80-85 a barrel by the end of Q2 FY27. Retail fuel prices would soften, perhaps with another central excise restoration as the Centre rebuilds fiscal space, and CNG hikes would slow. If the ceasefire holds only intermittently and the strait operates at reduced capacity, Brent would oscillate between $95 and $115, and Indian retail fuel prices would stay elevated through the festive quarter, putting pressure on the RBI’s June and August Monetary Policy Committee meetings. If the conflict escalates again — particularly if LNG infrastructure outside Ras Laffan is hit — gas pricing would tighten further, and CNG hikes would continue.

The Centre’s next decision points are visible. State VAT cuts, which the Centre has formally asked for, remain politically difficult. Bringing petrol and diesel under GST is on the agenda of the next GST Council meeting; the political odds are no better than they have been since 2017. A further excise cut would require fiscal space that the Budget for FY27 has not built in. The RBI’s June 3 to 5 meeting will be the first formal read on whether energy is changing the central bank’s inflation tolerance.

The conclusion most analysts skip

The Indian middle class will, in all probability, absorb this round of fuel hikes the way it has absorbed every previous one — with private grumbling, household-budget recalibration, and a slow shift in spending patterns away from discretionary items. There will be no movement, no protest, no organised political response. That stoicism is sometimes celebrated as resilience. It should also be read as a quiet signal to anyone willing to listen that the social compact between the Indian state and its urban earning class is being tested in ways that do not show up in any headline number. Fuel is the cleanest example. It is unavoidable, it is heavily taxed, it is globally exposed, and it is paid for in cash, every week, by people who get nothing visible back in return.

That is not a sustainable equilibrium. It is, for now, the equilibrium India is choosing. Whether it remains the equilibrium will depend less on what happens in the Strait of Hormuz over the next six months and more on whether any Finance Minister, Centre or state, decides that the time has come to rethink how India taxes the energy that the country runs on.