The numbers came in quietly, the way bad news usually does in India. On the morning of 26 May 2026, Indraprastha Gas Limited raised the price of compressed natural gas in Delhi by another two rupees a kilogram, to ₹83.09. It was the fourth such hike in twelve days. The day before, oil marketing companies had pushed petrol in Delhi to ₹102.12 a litre and diesel to ₹95.20, the highest since May 2022, after four increases in eleven days that together added nearly ₹7.5 to a litre of petrol. None of these revisions earned a banner headline. Stacked together, they tell the story of how a war four thousand kilometres away is being absorbed, slowly and unevenly, into the household budget of an autorickshaw driver in Sarita Vihar, a salaried executive in Gurugram and a delivery rider trying to pay rent in Noida.

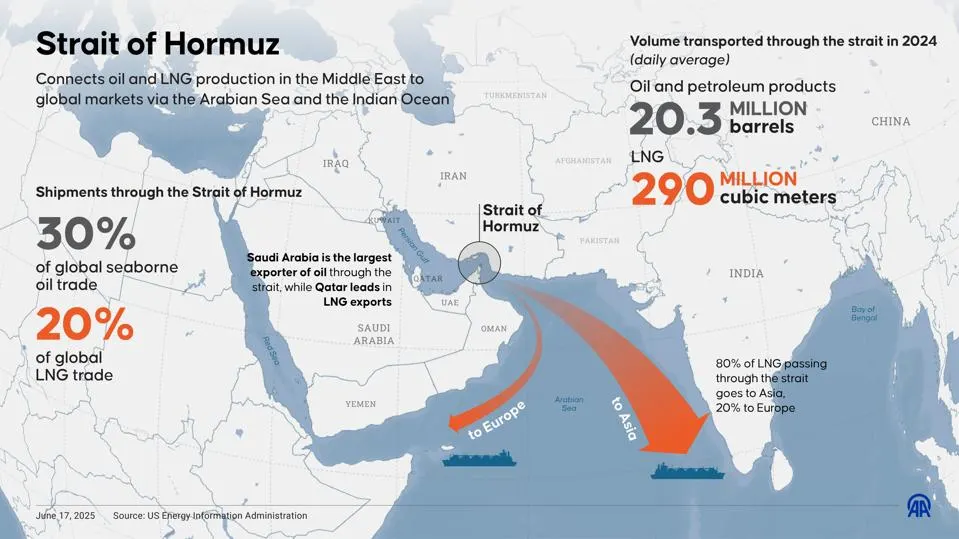

The war in question began on 28 February, when the United States and Israel launched a coordinated air campaign against Iranian military targets, an operation that, according to the House of Commons Library briefing on the conflict, included the killing of Iran’s Supreme Leader Ali Khamenei. Iran responded by shutting the Strait of Hormuz to all foreign shipping. The Islamic Revolutionary Guard Corps broadcast warnings on VHF radio that no ship was permitted to pass, then began boarding vessels and laying sea mines. The narrow stretch of water between the Musandam Peninsula of Oman and the southern Iranian coast, where the world’s most expensive cargo routinely transits in a sixty-kilometre corridor, became the single most disputed waterway on the planet.

By early May, only forty ships were crossing the strait in an entire week, against a pre-war average of about a hundred and twenty crossings every day, according to Lloyd’s List data cited by CNN. Iran began charging tolls of over a million dollars per ship to allow passage. The United States, after a failed round of talks in Islamabad, launched its own counter-blockade against Iranian ports on 13 April. By the time you read this, a conditional ceasefire was in place and a Pakistan-mediated framework was on the table, with American and Iranian officials discussing a roughly two-month extension during which the blockade would lift and the strait would reopen. Brent crude, which had crossed $110 a barrel on 20 May at the peak of the panic, had eased to about $98 by 26 May as those talks gathered momentum, according to Trading Economics.

That is the news. The deeper story is what it has cost India to be a country that imports nearly nine out of every ten barrels of crude it consumes.

What the strait actually does

The Strait of Hormuz is not a name most Indian readers grew up with, but it has been quietly central to their lives for two decades. The US Energy Information Administration, the standard reference for global oil flows, places the strait’s normal traffic at around 20.9 million barrels of oil a day in the first half of 2025 — roughly a fifth of all the petroleum liquids the world consumes, and about a quarter of every barrel that moves by sea. Roughly eighty-four per cent of the crude going through Hormuz is destined for Asia. India, China, Japan and South Korea are the four largest buyers. Liquefied natural gas flows on the same route, with most of Qatar’s LNG — the gas that fires Indian power stations, fertiliser plants and the kitchens of Delhi households on the city gas network — exiting the Gulf through the same passage.

Energy economists have long warned that no other waterway compresses so much consequential cargo into so narrow a space. Saudi Arabia and the United Arab Emirates have built bypass pipelines that can route some of their crude away from Hormuz; together those alternatives can move about 4.7 million barrels a day, helpful but well short of the twenty-million-barrel baseline. For Iran, this asymmetry has long been a strategic asset. It does not need to keep the strait closed to inflict damage. It needs only to make the global market believe closure is possible, and prices rearrange themselves.

Where India sits in the exposure map

India’s vulnerability is structural, and it is unusually well documented. The Ministry of Petroleum and Natural Gas, in its 2025-26 import statistics, places India’s crude import dependence at 88.6 per cent for the April to January period. Russia, which became India’s biggest supplier after the discounts that followed the Ukraine war, contributes around 31.5 per cent of crude imports by value. Iraq, Saudi Arabia, the United Arab Emirates and the United States make up most of the rest. The credit rating agency ICRA estimates that 45 to 50 per cent of India’s crude imports and between 54 and 60 per cent of its natural gas imports pass through Hormuz.

On LNG specifically, the concentration is harder to escape. India imported 27 million tonnes of liquefied natural gas in 2024-25, of which 11.2 million tonnes — roughly 41.4 per cent — came from Qatar, almost entirely from the Ras Laffan facility that was damaged in the early days of the war. Petronet LNG, India’s largest gas importer, issued a force majeure notice to QatarEnergy on 3 March 2026 on its long-term contract of 7.5 million tonnes a year. GAIL India warned downstream industrial customers of supply curtailments. For a few weeks in March, the country’s gas-fired power stations and fertiliser plants ran on a thinner margin than they had in years.

What followed was a hurried, improvised exercise in supplier substitution that revealed both the resilience and the limits of Indian energy logistics. Refiners reportedly raised the share of non-Hormuz crude in their basket from about sixty per cent to around seventy per cent within weeks, partly by leaning on Russian, American and West African cargoes. The US Treasury issued a thirty-day waiver permitting Indian refiners to buy stranded Russian crude and gas — an unusual concession that signalled how much Washington wanted Indian supply security held together. Domestic refinery output of LPG was ramped up by 36 to 38 per cent to take pressure off imports, according to the Petroleum Ministry’s mid-March briefing. On the LNG side, Shell India quietly became the country’s largest supplier in March and April, drawing on cargoes from Oman, Australia and Nigeria routed through its 5 million tonne per year terminal at Hazira in Gujarat. The Qatar gap got plugged, in other words, but only by buyers paying spot rates on longer-haul shipments and by Indian negotiators making calls at three in the morning.

What it has done to your money

Two transmission lines connect this Gulf disruption to the bills you are now paying.

The first runs through the rupee. The Indian currency touched ₹95.22 to the US dollar in March 2026, a low that the Reserve Bank’s foreign exchange interventions softened but did not prevent. A weaker rupee makes every dollar-denominated barrel more expensive in rupee terms, so even when Brent eased, the rupee did not catch up. By May, Reuters had quoted the rupee at around 96.96 to the dollar as oil and bond-yield strains continued. Every paisa of rupee weakness shows up, with a lag, on a petrol pump screen.

The second runs through inflation. The Ministry of Statistics released the April 2026 CPI print on 12 May, putting headline retail inflation at 3.48 per cent — the fastest annual pace in a year, and the fourth consecutive monthly rise. Food inflation climbed to 4.20 per cent. The transport index has so far been held flat by the Centre’s pre-emptive excise duty cut on 27 March, when the Special Additional Excise Duty on petrol was slashed from ₹13 a litre to ₹3, and on diesel cut to zero. That cut absorbed a meaningful chunk of the global shock. It did not, in the end, neutralise it. Four pump-price hikes in eleven days are the proof.

The Reserve Bank’s response so far has been to hold its benchmark repo rate at 5.25 per cent at the April Monetary Policy Committee meeting and revise its FY27 inflation projection upward to 4.6 per cent, nearly double the 2.1 per cent recorded in FY26. Governor Sanjay Malhotra noted, accurately enough, that India’s macroeconomic buffers in 2026 are stronger than in previous oil crises — forex reserves are large, the current account is manageable, the fiscal position is reasonable. Those are buffers against severity, not immunity from impact. The next MPC meeting is scheduled for 3 to 5 June. By then the committee will have one more CPI print, a clearer read on whether the ceasefire holds and a better sense of whether energy is going to do to FY27 what it last did to India in 2008 and 2011.

The reserves we forgot to fill

One uncomfortable fact has cut through the policy chatter of the past three months. India’s Strategic Petroleum Reserve — the underground rock caverns at Visakhapatnam, Mangaluru and Padur that exist precisely for moments like these — was only about 64 per cent full when the war began. The Minister of State for Petroleum and Natural Gas, Suresh Gopi, told Parliament in March that the SPR’s total capacity is 5.33 million tonnes and current holdings stood at roughly 3.37 MMT, enough for around five to ten days of consumption, depending on the metric used. Add the commercial inventories held by Indian Oil, BPCL and HPCL and you reach the often-quoted figure of 74 days of total stock. The International Energy Agency’s benchmark for its associate members is 90 days. Japan holds about 254 days. China holds between 110 and 140.

A Parliamentary Standing Committee report submitted in March urged the government to scale the SPR to the IEA’s 90-day standard. S.M. Vaidya, the former chairman of Indian Oil, told BusinessToday on 13 March that the country needs to “go aggressively” on reserve expansion, suggesting a target of around a hundred million barrels, which would give India something close to twenty days of strategic cover at current throughputs. The Centre has approved Phase II expansion at Chandikhol in Odisha (4 MMT) and a second cavern at Padur (2.5 MMT), but those are years away. The structural answer, in other words, was identified before the crisis and is being built after it.

What ordinary Indians are actually paying

The way this lands in a household is unspectacular but cumulative. Petrol in Mumbai sat at ₹111.21 a litre on 26 May. Diesel was ₹97.83. CNG in Delhi at ₹83.09 a kilogram had Noida and Ghaziabad consumers paying ₹89.7, and Gurugram at ₹86.12 before the latest revision. An autorickshaw driver who runs twelve hours a day on a tank of CNG is now spending about ₹400 to ₹500 a month more on fuel than at the start of May, on a fare structure that has not changed. A salaried family in Faridabad running one car and one scooter is paying roughly ₹2,000 more for the same commute. Food delivery companies have raised their base fares quietly. Airlines have stiffened fuel surcharges. Industrial gas allocations have been trimmed, which means fertiliser companies are paying more for the same ammonia output, a cost that will reach farmers and eventually consumers through the next kharif cycle.

And there is the human dimension that most analysts forget. Roughly nine million Indians live and work across the Gulf, sending home remittances that exceeded eighty billion dollars in 2024-25 across all source countries, according to RBI data. The crisis has not produced large-scale evacuations from Doha, Dubai or Manama, but Indian embassies in the region have issued advisories on contingency planning. For families in Kollam, Malappuram, Aligarh and Gulbarga who depend on those monthly transfers, every escalation is a quiet anxiety that does not show up on a market dashboard.

What most reports are missing

The dominant frame in daily coverage has been crude oil. The under-reported angle is gas. India spent two decades patiently diversifying its crude basket — Russian discounts, American shale, West African and Latin American cargoes — and that diversification has paid off in this crisis. India’s LNG architecture, however, has remained heavily tied to long-term Qatari contracts that exit through the same strait. When Ras Laffan was hit and Petronet declared force majeure, there was no equivalent diversification ready to plug the gap immediately. The spot LNG market is small relative to oil. The fleet of LNG carriers globally is constrained. Long-term contracts with the United States and Australia are now in faster negotiation, but new infrastructure takes years. This concentration in gas supply is the under-discussed structural vulnerability that the 2026 war has exposed, and it is the one most likely to shape Indian energy policy for the rest of the decade.

The second missing angle is the SPR fill rate. A reserve that exists is one thing. A reserve that is two-thirds full when a war breaks out is another. Parliament has now been told. The political question is whether the next Union Budget will fund the gap.

What happens next

Three trajectories are worth tracking through the second half of 2026. In a successful de-escalation, the ceasefire is extended, the US lifts its naval blockade, Iran reopens the strait, insurance premiums normalise and Brent settles into a $75 to $90 range. Indian retail fuel prices ease gradually, perhaps with another excise duty restoration as the Centre rebuilds fiscal space. In a partial-disruption scenario, the ceasefire fractures intermittently, the strait operates at half capacity, Brent oscillates between $95 and $115, and Indian fuel prices stay elevated through the festive season. In a worst-case scenario, the conflict widens to other Gulf countries or to additional LNG infrastructure, Brent runs past $130, and the Reserve Bank, the Ministry of Finance and oil marketing companies face the kind of trilemma between inflation, growth and household pain that India last navigated in 2008.

What we have learnt by 26 May is that even a partial closure of Hormuz, even a temporary one, is enough to push CPI, the rupee, the repo rate and a Delhi CNG pump in the same direction at the same time. Energy security has stopped being a foreign-policy abstraction. It is now a household variable. The petrol pump in Patna and the shipping lane off Bandar Abbas are connected by a logic the average citizen never signed up for and cannot escape.

The honest conclusion is uncomfortable. India will get through this crisis. It always does, with a mix of supplier diversification, fiscal cushioning, central-bank discipline and the quiet endurance of the Indian middle class. What India should not do is forget, the way it has forgotten after every previous Gulf shock, that the world will give us another one. The reserves should be filled. The LNG basket should be diversified. The shipping insurance architecture should be domesticated. The renewables and storage roll-out should be accelerated, not because climate goals demand it, which they do, but because energy independence is now national security. The petrol pump display is the most democratic information system in this country. It tells the truth, in rupees and paise, every morning. We should listen to it more carefully when the war is over than we did when it began.